There are multiple ways to set up a private equity fund. The most common types are described here.

FUND STRUCTURES

Whole Fund Model

Under the “Whole Fund” or “Blind Pool” model, investors purchase interests in a pooled investment fund (the Fund), which is usually formed as a limited liability company (LLC) or a limited partnership (if you are including Non-U.S. investors). For purposes of this article, we will assume the structure is a Manager-managed LLC with two classes of members (Class A and Class B Members). The Fund will be the sole or partial owner of multiple assets (Assets).

The Fund will form a new, subsidiary entity to hold title to each new Asset in which the Fund invests. Bank loans will occur at the Asset level, which is also where all operating expenses and debt services will be paid and any required lender reserves will be held. Periodically, excess cash will be swept from the Asset bank account to the Fund bank account, where cash from all Assets are pooled prior to determining “Distributable Cash” (after-expense cash flow) to the Fund’s Class A and Class B Members. Asset Management Fees may be paid to the Fund Manager at the Asset level or from the Fund as described in the respective Operating Agreements for the Fund and each Asset. In the Whole Fund model, investors share in profits and losses associated with all of the Fund’s Assets, and distributions are calculated after aggregating cash from all of the Assets.

Deal-by-Deal Model

The “Deal-by-Deal” model is similar to the Whole Fund model in that all investors invest in the Fund; however, instead of aggregating cash prior to making distributions, Distributable Cash is calculated separately for each Asset and then aggregated. This could create a situation where the Fund Manager receives distributions from performing Assets, even while other Assets are not performing. To mitigate this effect on Fund investors, a “clawback” of excess Manager distributions may be required if certain preferred returns or other investor returns haven’t been met in the aggregate.

Advantages of Both Fund Models

The above models offer diversity to investors and allow you to raise money before you have an Asset identified. However, private equity companies and family offices seem to be reluctant to invest in a pooled investment fund. To overcome this objection, a correctly structured Whole Fund or Deal-by-Deal Fund should offer sufficient flexibility that private equity and family office investors can co-invest with the Fund at the Asset level without becoming Members of the Fund.

From a cost perspective, each of the above Fund models will require initial setup fees for a PPM, Fund Operating Agreement, Subscription Agreement and the “Investment Summary” describing your business model; plus, you will need new single-purpose entities set up for each Asset, as well as securities notice filings. As these documents are significantly more complex than a Specified Offering (described below). It will cost more to set up a Fund than to set up a Specified Offering.

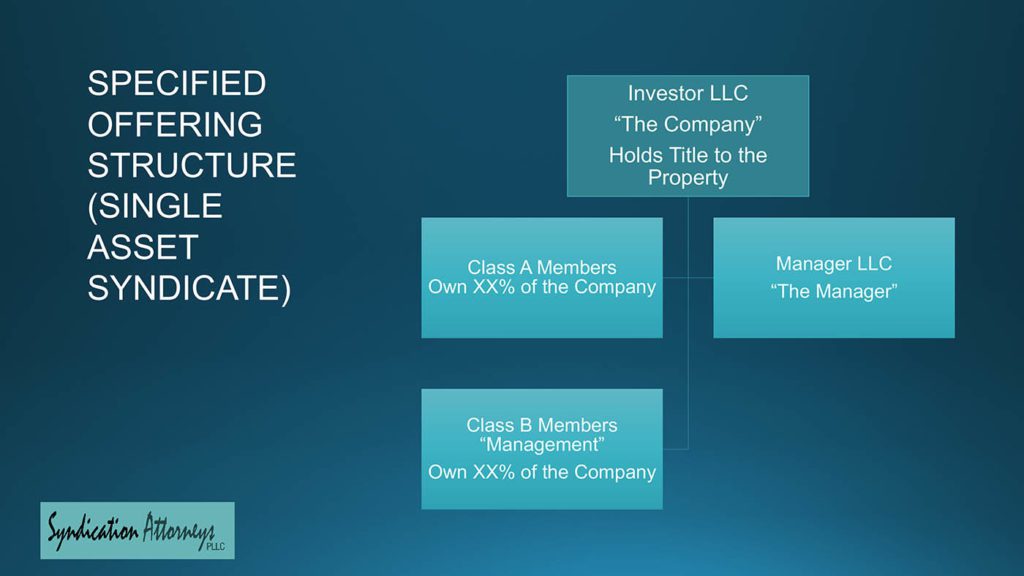

Specified Offering Model

The Specified Offering Model is based on raising funds to acquire a specific Asset. For this model, each Asset will have a separate PPM (if needed), an LLC Operating Agreement that will hold title to the Asset and sell interests to investors, a Subscription Agreement, and securities notice filings. Funds are raised for a specific deal, with separate investors in separate Assets, although it is possible to do a multi-Asset specified offering when the Assets have been identified prior to launching the offering. The advantage of this model is that it is the easiest way to raise money, as investors like to invest in tangible things versus investing in your business model and trusting you to invest in Assets that meet your criteria.

From a cost perspective, you will incur initial setup fees for the PPM, LLC Operating Agreement, Subscription Agreement, and securities notice filings for each Asset you acquire. Despite the additional costs, this model works because it is often easier to get investors to invest in specific Assets than it is to get them to invest in a Fund. Thus, it is the easiest way to raise money. And don’t forget, your legal and organization expenses are reimbursable if you build them into your fund raise.

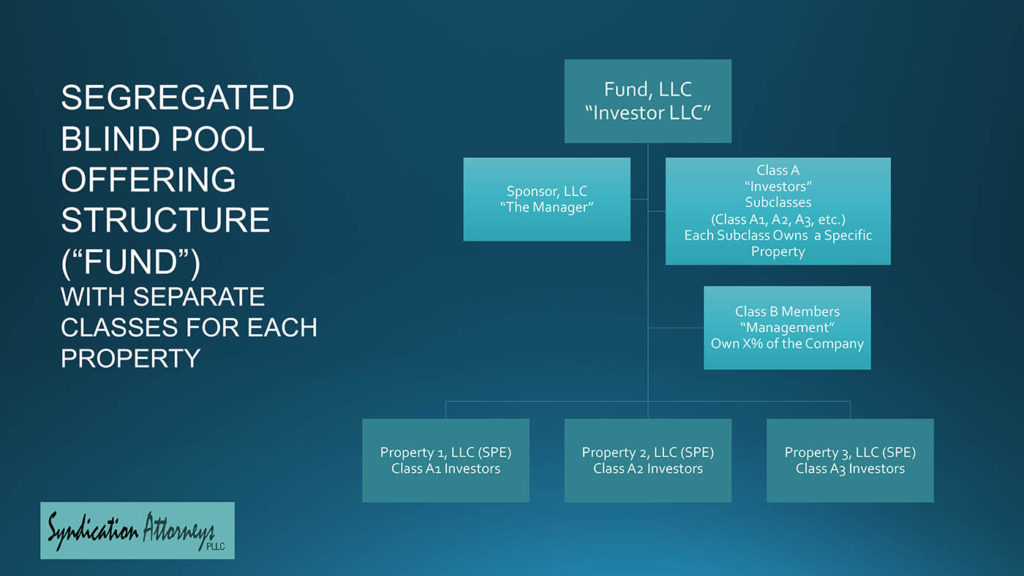

Hybrid Segregated Offering Model

A “Segregated Offering” model is a hybrid of the Fund concept described above (based on your business model) and the “Specified Offering” model (based on a specific Asset). For this model, each Asset will be acquired by a separate “class” in the investor-level LLC or perhaps a separate investor-level LLC formed to acquire each Asset.

In both variations, funds are raised deal-by-deal, with separate investors in separate Assets. This is not a true “Fund” model, as investor funds and Assets are not aggregated, but rather it is a series of separate offerings under a single PPM. The advantage of this model is that it prevents having to draft the PPM for each new investment. However, from an SEC perspective, all separate offerings under a single PPM will still be considered to be part of the same offering.

From a cost perspective, you will incur initial setup fees for the PPM and your “Investment Summary” describing your business model; plus, you will need new Asset-level entities as well as deal-specific amendments or supplemental documents for each Asset, so each Separate Offering will require its own fees. Despite the additional costs, this model works because it is often easier to get investors to invest in specific Assets than it is to get them to invest in a Fund.

Summary

In summary, the best deal structure is that one that allows you to raise money for your stated business purpose. Those who are starting out should consider doing a series of Specified Offerings to build a track record. Those with substantial experience in a specific Asset class or with previous securities offerings can do successful Fund Offerings.

We can help with any of these structures; and we can help you choose the Fund Structure that is best for you.