Why Does it Matter and How Does One Get Verified as Accredited?

When must investors in a syndication deal be Accredited, and when can Non-Accredited Investors participate in the opportunity? Sometimes the answer is not clear-cut, which is why it’s always a good idea to consult with a Securities Attorney. Before delving into that question, let’s consider different levels of investor qualifications.Who are “Accredited Investors”?

The U.S. Securities and Exchange Commission provides eight standards that an Accredited Investor must meet. The term Accredited Investor is defined in Rule 501 of Regulation D (17 CFR 230.501(a)) and includes any person who comes within any of the following categories, or who the issuer reasonably believes comes within any of the following categories, at the time of the sale of the securities to that person:- Any bank, savings and loan association; securities broker or dealer; insurance company; registered investment company or business development company; SBA licensed Small Business Investment Company, certain state or government employee benefit plan with total assets in excess of $5,000,000; any employee benefit plan if the investment decision is made by a plan fiduciary that is either a bank, savings and loan association, insurance company, or registered investment adviser, or if the employee benefit plan has total assets in excess of $5,000,000 or, if a self-directed plan, with investment decisions made solely by persons who are accredited investors;

- A private business development company;

- Any non-profit organization, business trust or partnership, not formed for the specific purpose of acquiring the securities offered, with total assets in excess of $5,000,000. Note: per 17 CFR 230.501(e)(2), a corporation, partnership or other entity shall be counted as one purchaser. If, however, that entity is organized for the specific purpose of acquiring the securities offered, then each beneficial owner of equity securities or equity interests in the entity shall count as a separate purchaser;

- Any director, executive officer, or general partner of the issuer of the securities being offered or sold, or any director, executive officer, or general partner of a general partner of that issuer;

- Any natural person whose individual net worth, or joint net worth with that person's spouse, exceeds $1,000,000, except that:

- The person's primary residence shall not be included as an asset;

- Indebtedness that is secured by the person's primary residence, up to the estimated fair market value of the primary residence at the time of the sale of securities, shall not be included as a liability (except that if the amount of such indebtedness outstanding at the time of sale of securities exceeds the amount outstanding 60 days before such time, other than as a result of the acquisition of the primary residence, the amount of such excess shall be included as a liability); and

- Indebtedness that is secured by the person's primary residence in excess of the estimated fair market value of the primary residence at the time of the sale of securities shall be included as a liability;

- Any natural person who had an individual income in excess of $200,000 in each of the two most recent years or joint income with that person's spouse in excess of $300,000 in each of those years and has a reasonable expectation of reaching the same income level in the current year;

- Any trust, with total assets in excess of $5,000,000, not formed for the specific purpose of acquiring the securities offered, whose purchase is directed by a sophisticated person; and

- Any entity in which all of the equity owners are accredited investors.

So why do Investor qualifications matter?

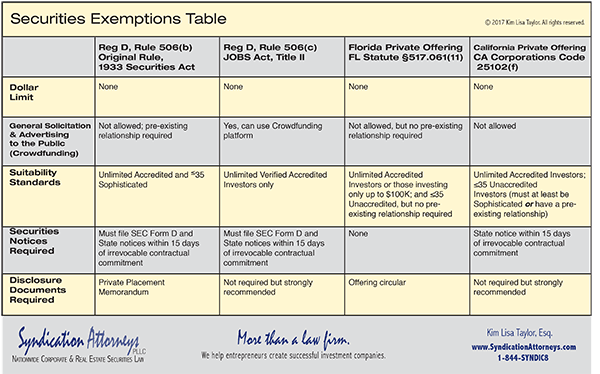

Because before anyone can sell securities (i.e., promissory notes or investment contracts) to private investors, they must either register the investment (by getting regulatory pre-approval to make a “public offering”) or by qualifying for an exemption from registration. The exemption you choose will determine: a) the financial qualifications of your investors, b) whether you can advertise or if you can only offer the opportunity to people with whom you have established a substantive pre-existing relationship, and c) what kind of risk disclosure document, if any, you need to provide. In addition, most exemptions require some type of filing with federal or state securities regulators (or both) notifying them which exemption you are claiming and giving them jurisdiction over you in case you do it wrong. Securities exemptions exist at the state or federal level. The most commonly used exemption is federal Regulation D, Rule 506, which is further divided into Rule 506(b) or 506(c). There are also intrastate exemptions that may be available for some offerings where everything — the issuer, the property and investors — are all in one state. Included here is a table summarizing the requirements of the most common federal securities exemptions and the Florida and California Private Offering Exemptions:

How does one prove he or she is Accredited?

Let’s suppose an issuer has selected the Regulation D, Rule 506(c) exemption which requires that investors be verified as Accredited. How, then, does one become verified, or otherwise prove that he or she is Accredited? In the case of Regulation D, Rule 506(b) Offerings or for the Florida or California private offering exemptions shown in the table, investors can self-certify by answering a set of questions (usually in the Subscription Agreement that accompanies the offering documents) designed to see whether they meet one of the SEC's eight definitions of an Accredited Investor or if they meet one of the other qualifications for a specific offering of securities. For Regulation D, Rule 506(c) Offerings, self-certification is not sufficient, as the Issuer of the Securities has to be "reasonably assured" that each investor is Accredited. The following are some non-exclusive examples of how an investor can be verified as Accredited per 17 CFR 230.506(c)(ii): (A) Qualification on the basis of income can be had by reviewing any IRS form that reports the purchaser's income for the two most recent years (such as Form W-2, Form 1099, Schedule K-1 to Form 1065, and Form 1040) and obtaining a written representation from the purchaser that he or she has a reasonable expectation of reaching the income level necessary to qualify as an Accredited Investor during the current year; (B) Qualification on the basis of net worth can be had by reviewing one or more of the following types of documentation dated within the prior 90 days and obtaining a written representation from the purchaser that all liabilities necessary to make a determination of net worth have been disclosed:(1) Assets: Bank statements, brokerage statements and other statements of securities holdings, certificates of deposit, tax assessments, and appraisal reports issued by independent third parties; and

(2) Liabilities: A consumer report from at least one of the nationwide consumer reporting agencies; or

(C) Obtaining a written confirmation from someone with a license asserting that they have taken reasonable steps to verify that the purchaser is an accredited investor within the prior 90 days and has determined that such purchaser is an Accredited Investor. Such persons include:(1) A registered securities broker-dealer;

(2) An investment adviser registered with the SEC;

(3) A licensed attorney in good standing; or

(4) A certified public accountant in good standing.

(D) In regard to any person who purchased securities in an issuer's Rule 506(b) offering as an accredited investor prior to Sept. 23, 2013, and continues to hold such securities, for the same issuer's Rule 506(c) offering, obtaining a certification by such person at the time of sale that he or she qualifies as an accredited investor. Because each exemption has its own set of rules, this is where an experienced securities attorney can be invaluable. An experienced securities attorney can help you determine which exemption is the best fit for your circumstances as well as help you fully understand and comply with its requirements. Further, he or she will offer structuring advice regarding how you should split profits with investors and the appropriate investment contract to use with investors for the type of assets your syndicate is acquiring. Without this counsel, you are likely to misstep, and the consequences can be dire, both for the issuer and its investors.